Perpetual Markets Economics and Interest Rate Commentary – 4 May 2026

RBA widely expected to increase interest rates again this week. I favour a hawkish hold due Middle East uncertainty, though new peace proposal received on Friday. Australian interest rates ultimately headed higher.

Key points

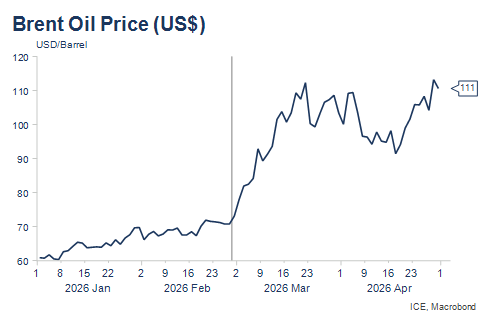

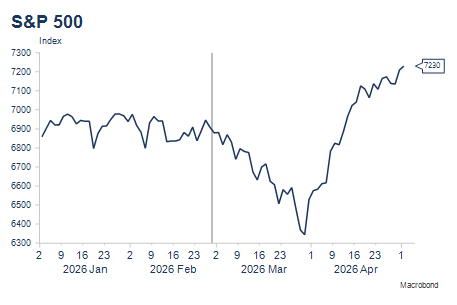

- Another week and the Strait of Hormuz is still closed, though negotiations continue, with a further peace plan proposed by Iran, which is encouraging. The US share market has made another record high as earnings from the AI boom and expected future profit growth propel major tech stocks higher.

- The RBA Board meeting on Tuesday and updated forecasts are the focus of attention for Australia this week. The market is three quarters priced for another rate rise and economists for the most part agree. Given the closeness of last month’s decision, and the continuing uncertainty in the Middle East, there is a case to wait for more information. It wouldn’t take much to swing last month’s 5-4 vote to tighten in the other direction. The RBA meeting is previewed in full below. I’m still coming down on the side the Board will vote to pause, even though I think RBA staff will recommend an increase to the Board and further interest rate rises will be likely in the months ahead, if the conflict is resolved.

- There will also be interest in ANZ job ads and the Melbourne Institute’s Inflation gauge to be released on Monday, and the Household Spending Indicator (Tuesday), both of which might provide some early signs of how the Iran conflict is impacting the economy. The HSI now includes spending on petrol, which is why economist forecasts are strong. The RBA’s business liaison program will have additional insight on the economy, though this information is not available to the market.

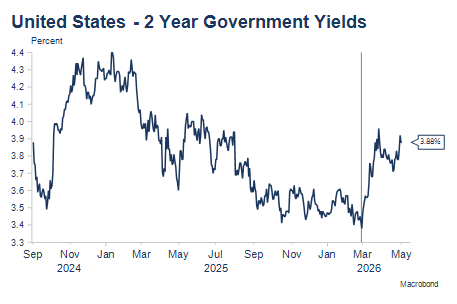

- The past week saw the beginnings of a shift in the bias on US interest rates to neutral from easing, pushing US 2-year yields 10bps higher. Those FOMC members wanting to signal the next move could as likely be up as down, are clearly more worried about inflationary pressures, while several members, remain concerned about labour market risks.

- This week culminates with the release of April US non-farm payrolls on Friday, where a smaller gain of 62K is expected after last month’s bounce back +178K. Before that both Job Openings and Challenger Layoffs are released. I see the risk as being slightly to the upside on employment this month, notwithstanding recent geopolitical developments. The unemployment rate is seen unchanged at 4.3%. No employment growth is consistent with stable employment growth such has been the reduction in net immigration!

- Elsewhere, it’s worth noting The Economist had an article in its latest edition entitled “Oil markets are still in La La land”. This makes similar arguments to which we have been advancing that much higher oil prices will be required to destroy the 20% of global demand that cannot be supplied, in the event of an extended Strait of Hormuz closure. Prices should be able to return to close to pre-conflict levels and the more favourable outlook for the economy re-establish, if a peace agreement can be reached.

RBA preview - background and context

The RBA’s Monetary Policy Board meets on Monday and Tuesday, with any change to the official cash rate announced at 2.30PM AEST on Tuesday.

The Board will be provided with updated economic and inflation forecasts from RBA staff, along with recent feedback from companies participating in the RBA’s business liaison programme. The latter information is not public and could be important in the current environment when developments in the economy will be running well ahead of the published economic data.

The RBA’s February economic forecasts did not foresee inflation returning to near the 2.5% midpoint of the RBA’s target band until mid-2028. These forecasts incorporated the assumption of two interest rate increases, which have already been enacted (in February and March). Even after these moves, the time of the return to target was unlikely to be acceptable to the Board given the prior extended period of above-target inflation. That suggested a further increase in interest rates was highly likely in the months ahead, quite likely at the May Board meeting following confirmation of elevated inflation and low unemployment in data released during April, if the impact of the Middle East situation did not have to also be considered.

Communications from RBA senior staff during April (Deputy Governor Hauser in New York and Assistant Governor Hunter in Washington) were hawkish. This probably suggests the board paper recommendation will be for a further interest rate rise at the May meeting, though the communications might also reflect an attempt to contain inflationary expectations during this period of elevated energy prices.

The Iran conflict and the March RBA decision

It is worth re-reading the March Board Minutes to refresh the debate that occurred at that meeting between tightening further and waiting further information: 17 March 2026 | Minutes of the Monetary Policy Board Meeting | RBA.

The March decision to raise interest rates was of course made by a narrow 5-4 majority vote. Those voting to keep interest rates on hold were concerned about the increased uncertainty from the current conflict and less convinced that developments in economic indicators since February were inconsistent with the February forecasts. Importantly, this minority also concluded that while further tightening was likely to be necessary soon, there was merit in waiting for additional information about the course of the Iran conflict, given the potential negative impact on demand and unemployment, depending on how the conflict developed.

The majority that favoured increasing interest rates, were more concerned about the need to prevent medium-term inflationary expectations from rising, thought that the labour market remained inconsistent with at-target inflation, and that monetary policy settings were likely not sufficiently restrictive to return inflation to target.

The decision on Tuesday

Two months into the conflict, while a ceasefire continues, oil prices remain very elevated and at the time of writing, the Strait of Hormuz remains closed. An end date for the conflict is unclear. Bookend outcomes range between a very extended closure of the Strait of Hormuz, which would likely result in much higher oil prices, fuel shortages and rationing, and global recession, to a swift resolution, which would likely allow the previous improving outlook for the world and Australian economies to re-establish.

Given the wide uncertainty about that range of outcomes, and the further interest rate rise already delivered in March, there is reasonable likelihood that those that favoured awaiting further information on how the conflict might play out in March, continue to hold that view. The sharp falls in consumer confidence and business confidence during March and early April, portend negative developments in the economy, unless the conflict ends soon and oil prices revert nearer to pre-conflict levels. Provided the conflict ends, a further two interest rate increases are likely this year.

At the same time, it’s likely the two RBA members of the Board will vote for a further increase in interest rates given senior staff comments in April, both to ensure that monetary policy is sufficiently restrictive to return inflation to target over the medium-term and possibly to achieve that outcome a little quicker than forecast in February.

This suggests it could be another close vote on Tuesday, with another 5-4 vote in favour of an increase possible. By the same token, it would take only one member that voted to tighten last time to now favour waiting for further information, to produce a 5-4 vote in the other direction!

If it was me…

Increasingly, and to an extent with the benefit of hindsight, I am of the view that the RBA should have tightened policy a bit further coming out of COVID and prioritised lowering the rate of inflation earlier. There was little danger of raising unemployment in the early years with so much excess demand for labour, while the significant increase in the cost of living and cost of doing business has been detrimental to almost all Australians.

Given this, I would ordinarily argue that a further interest rate increase should be implemented in May to increase my confidence that the inflation rate would moderate to 2.5% and preferably a little earlier than the mid-2028 timeframe foreshadowed in the February forecasts (pre-Iran), with a further rate rise likely to follow also later in the year.

However, given the initial impacts on confidence and auction clearance rates, and the likely significant additional negatives for the economy that would develop in the case of a very extended closure of the Strait of Hormuz, I don’t see significant cost in waiting until the next meeting or the one after before implementing further tightening. A 4.35% cash rate is unlikely to cause the Australian economy or businesses too much stress if oil prices return to near pre-conflict levels. On the other hand, a 4.35% cash rate with US$150-200pb oil would be a very different matter, especially if fuel supplies were also interrupted. Six to ten weeks won’t significantly change the length of time over which inflation returns to target relative to the current mid-2028 expectation, but it could add additional unrequired restrictiveness to the economy in the case of an extended disruption to oil supplies.

Middle East developments and chart review

Oil prices have risen to new highs for the crisis over the past week as the Strait of Hormuz remains closed. Peace talks do not appear to be progressing, however, at least the two sides are making proposals, which is an important step to an outcome in any negotiation. The longer the substantial proportion of the global supply of oil, LNG and other inputs including resin and fertiliser remains out of the market, the greater the risk of sharp price spikes due to shortages. The Economist this week suggests oil markets are in “La La land”, and there is considerable risk of much higher prices than priced. This is the reason I would wait for further information if I was on the Reserve Bank Monetary Policy Board, as the world and Australian economies could end up in a very different economic situation relatively quickly, if the supply interruptions drag on.

Reflecting continuing strength in US corporate earnings, particularly among tech stocks due to the AI boom, the US share market made further new record highs last week. That’s a reminder of the double shocks impacting the world economy presently and of the cushioning effect of AI spending on growth despite much higher oil prices.

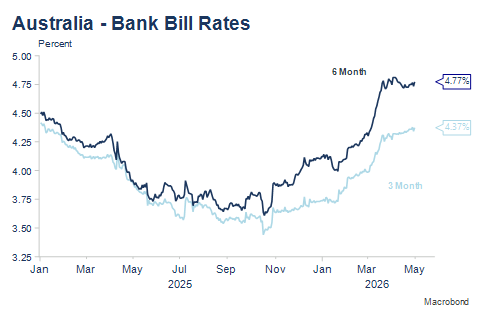

With the RBA Board very widely, but not unanimously, expected by economists to raise interest rates again on Tuesday, Australian short-end yields have ticked up a few points this week. The market is pricing a total of just over two and a half further rate increases this year, with a near 75% probability attached to a move this week. That quantum of rate increases would be unlikely to be necessary if oil prices remain around current levels or rise further.

Meanwhile, US short-term yields continue to price a very small risk of one rate cut this year, and a very small chance of a rate rise next year. Two-year yields have risen around 10 basis points over the past week. The divide in pricing captures the emerging shift in the FOMC’s bias toward neutral – where interest rates might as easily rise as fall – and the divide in concerns between Fed members between inflation and employment.

Economic Calendar – key Australian and US events this week

Monday 4 May: ANZ Indeed Job Ads (April); Building Approvals (March); Melbourne Institute Inflation Gauge (April).

Tuesday 5 May: RBA Board Meeting, Statement on Monetary Policy and Press Conference; Household Spending Indicator (March); (overnight) Non-Manufacturing (Services) ISM (April); Job Openings (April).

Thursday 7 May: (overnight) Challenger Layoffs (April).

Friday 8 May: (overnight) US Non-farm payrolls (April); Unemployment Rate (Apri); University of Michigan 5–10-year inflationary expectations.

There are also 10 of 19 FOMC members listed to speak, including two of the three voters that dissented in favour of a balanced or neutral interest rate directive, instead of one with an easing bias.