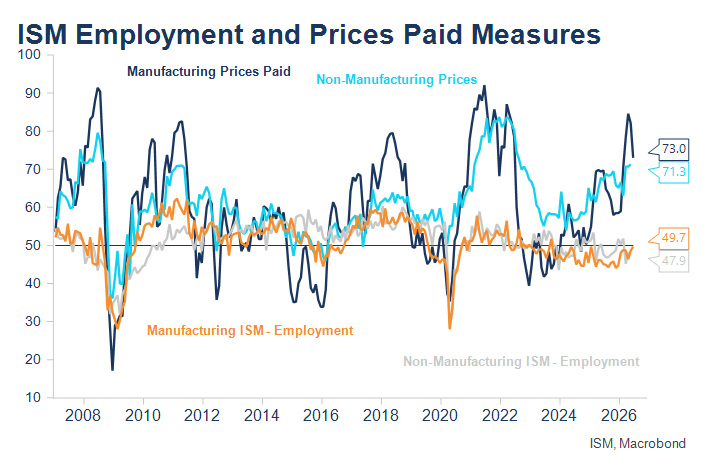

ISM Services Employment series important to see whether AI growth momentum re-establishes and near-term inflationary pressures subside following end of conflict

Key points

- I’m looking for employment indicators to improve and inflationary pressures to decline in coming months, following the end of the US/Iran conflict. Tonight’s Services ISM employment result is important in this regard, as are coming months’ results.

- If correct, this should see the re-emergence of an elongated tightening cycle as dynamics associated with the ongoing AI investment boom re-establish, supporting growth and boosting inflation in the near- to medium-term. Longer-term implications for employment remain uncertain.

- FOMC Minutes of interest and likely shorter in keeping with a reduction in Fed communication since Chair Warsh took over.

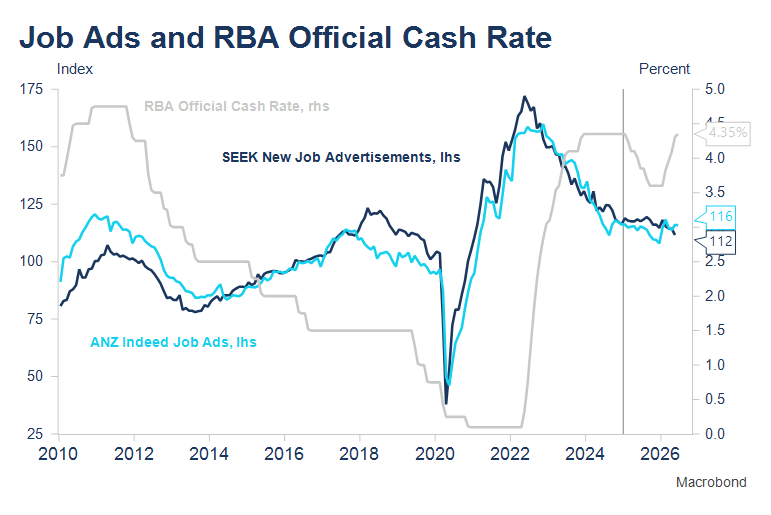

- ANZ Indeed Job Ads important this morning to see if there is confirmation of a slight trend decline in SEEK job ads, which might signal that the next move in Australian interest rates is down. That said, recent moves likely reflect higher oil prices rather than higher interest rates to date, meaning a reversal in coming months might well occur.

Macroeconomic and interest rate outlook – base case

The key elements shaping the near-term economic and interest rate outlook in the US and Australia are/have been:

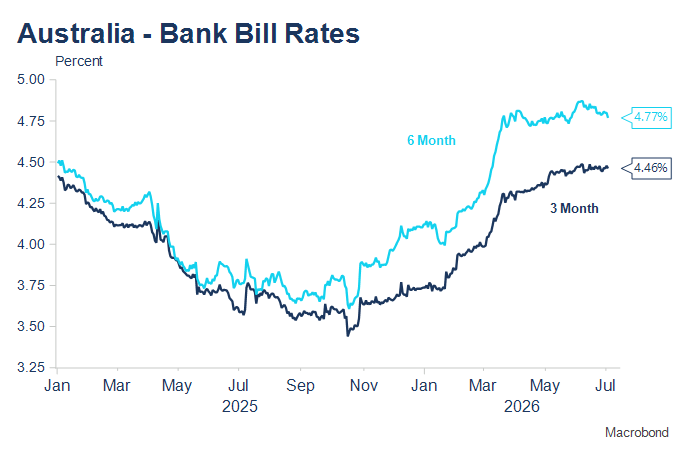

- Continuing above-target inflation. The RBA has moved to address this issue with three interest rate increases in H1, but the Fed has yet to make any alteration to monetary policy.

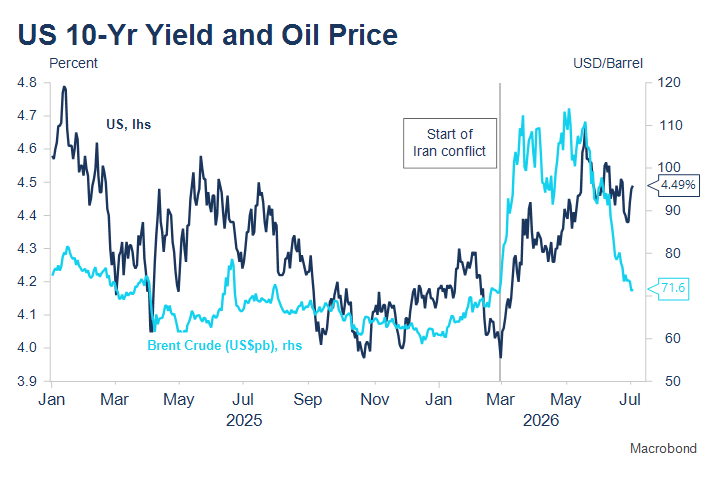

- Oil prices and supply chain disruptions for a number of commodities due to the closure of the Strait of Hormuz. This source of near-term inflationary pressure for both economies and the globe is normalising more quickly than expected, though to date, shipping movements through the Strait remain well below pre-conflict levels.

- The AI investment boom. This did not end because of the Iran conflict and remains an important support for economic growth in many countries in the near- to medium-term as data centres are rolled out globally. There are associated near-term capacity constraints and inflationary pressures evident in copper, electricity and water supply and semi-conductors, such is the scale of the boom, while the longer-term impact on employment remains uncertain.

More recently, taxation changes in the Australian budget have added to the existing negative fundamentals pressuring the Australian housing market.

My base case has been that a relatively quick (measured in months) resolution to the Middle East conflict would see oil prices retreat and supply conditions normalise relatively quickly, allowing the prior emerging strength in AI investment to support growth around the world, particularly in the US and Asia. In the short-term, price pressures would reverse quickly as fuel surcharges were removed and supply constraints unwound much more quickly than during the COVID pandemic, when longer-term disruptions had occurred and demand was far stronger, supported by very low interest rates and very accommodative monetary policies globally.

The associated improvement in global demand due to continuing AI investment however, would also be accompanied by other inflationary pressures, meaning the most likely scenario for interest rates was a long slow tightening cycle, as occurred during the mid-2000s when Australia experienced a mining boom and the US, its ill-fated housing boom.

The above remains my core scenario, though recent and prospective moves by central banks to combat continuing above-target inflation will likely mean some interest-sensitive areas of demand, especially housing, are headwinds to growth. Though broader construction cycles will likely remain supported by spending on AI, renewables, defence and selected parts of mining.

How to track whether this scenario is unfolding

In the US, I have been relying heavily on the signals of the ISM indicators and the Indeed Job Openings series over much of the past two years, initially following the imposition of US tariffs, though the same indicators have proved equally relevant since the advent of the US/Iran conflict.

The ISM charts show that quite differently to the pandemic experience, while prices have unsurprisingly accelerated, employment conditions have softened, importantly, interrupting improving trends in evidence ahead of the Iran conflict. For my core scenario to be correct, I’m expecting to see the ISM prices paid indicators retreat sharply in coming months, while the employment indicators recover over the same period. There’s an important update on Services Employment tonight (manufacturing employment improved close to the important 50 mark in June, while prices paid have begun to decline). One important note is that there may be a couple of months where payrolls print softer as a result of the impact of the temporarily higher oil prices since late February. That was evident in the June non-farm payrolls data.

In Australia, I continue to follow the signals of job ads and the NAB Business Survey, my two favourite indicators of the Australian economy. SEEK job ads have begun a slight trend decline, which if sustained could signal that the next move in interest rates is indeed down as three of Australia’s four major banks now predict. However, the signal has not been confirmed by the ANZ Indeed job ads series, including with the June data which was released this morning at 11.30am AEST.

In the US, it’s likely too early to see any recovery in employment intentions as yet, and perhaps some further easing might occur this month. Different to the US, Australian data may also be impacted by the increases in interest rates in February, March and May, though my assessment is that any more recent developments are related to oil prices rather than interest rates. How business conditions develop in the NAB Survey, again probably more from the July survey than next week’s June release, will provide a gauge as to the impact on the Australian economy from higher oil prices versus higher interest rates.

The week ahead – ISM Services Employment, FOMC Minutes, ANZ Job Ads, RBNZ and RBA’s Hunter speech the key events

Monday 6 July

- 00am AEST Melbourne Institute Inflation Gauge (June)

- 30am AEST ANZ Indeed Job Ads (June)

- Midnight AEST ISM Services PMI (June)

Wednesday 8 July

- 00 am AEST RBA Hunter speech at Australian Conference of Economists’ session on “Supply shocks and their implications for monetary policy”

- 00am AEST $900m 4.25% 2036 tender

- 00pm AEST RBNZ Official Cash Rate Review (a rate rise is 75% priced).

- 00pm AEST RBNZ Governor Press Conference

Thursday 9 July

- 00am AEST FOMC Minutes June

- 00am AEST $150m 0.25% 2032 indexed bond tender

Friday 10 July

- 00am $900m 1.75% 2032 bond tender

While it’s a sparser calendar of significant economic data and events this week, there are important updates on key variables shaping my strategic view of the emergence of a long slow tightening cycle in both the US and Australian economies. The RBA’s Hunter speaks in a conference session on the implications of supply shocks for monetary policy. Some key aspects of what other central bankers have said on that topic include:

- Central banks cannot fix supply shocks.

- Temporary supply shocks should be looked through (ignored), however, a sequence of supply shocks or a very large supply shock should not be ignored if there are signs of broad-based inflationary pressures or there are risks of inflationary expectations becoming de-anchored.

The US/Iran conflict certainly seems to fit into the category of temporary supply shocks, though the continuation of above-target inflation for many years in both Australia and the US can be considered as raising the risk of inflationary expectations becoming de-anchored.

The RBNZ is widely expected to lift NZ interest rates, though a move at this meeting is only 75% priced, and several major NZ financial institutions see the RBNZ on hold again. The uncertainty perhaps reflects the possibility that RBNZ members again vote as a bloc and the Governor again uses her casting vote in favour of a hold, as she did in May. At that time, a hike later in 2026 was signalled, but contained core inflation and ongoing elevated unemployment was also a consideration. The fact that the Middle East conflict looks to have been removed as an inflationary force may be a reason to again resist raising interest rates at this meeting.

The publication of the June FOMC Minutes early on Thursday morning AEST is keenly awaited to see any evolution in the detail of the Meeting provided after Chair Warsh signalled a review of Fed communications at his first press conference. In keeping with Warsh’s view that too much communication reduces important market signals, since that press conference there have been far fewer speeches by Fed officials (just two appearances are scheduled this week according to Bloomberg). I suspect the most likely development at this stage will be shorter Minutes, as there still needs to be a record of the FOMC Meeting. There may be more changes after the Communications Task Force reports later this year.

I’ve only singled out three pieces of data to focus on this week. In keeping with the earlier section on the macroeconomic outlook, the ISM Services employment question is seen as the most important. It will be important for my strategy that services employment intentions recover over coming months as fuel prices drop.

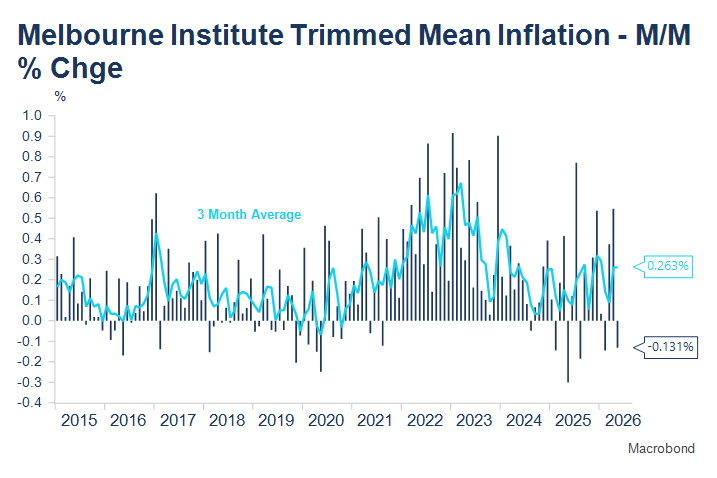

In Australia, there are two relatively interesting data updates. The Melbourne Institute Inflation gauge provides the first indication of price developments in June, important input ahead of the June quarter CPI later this month. The NAB Survey pricing indications will also be important next Tuesday, but fuel prices have obviously dropped sharply in recent months, so readings in July and August are likely to be even more important. March and April trimmed mean readings were very elevated but May saw a fall; something that has been a regular occurrence in the second month of the quarter in recent times.

Australian interest rate market developments

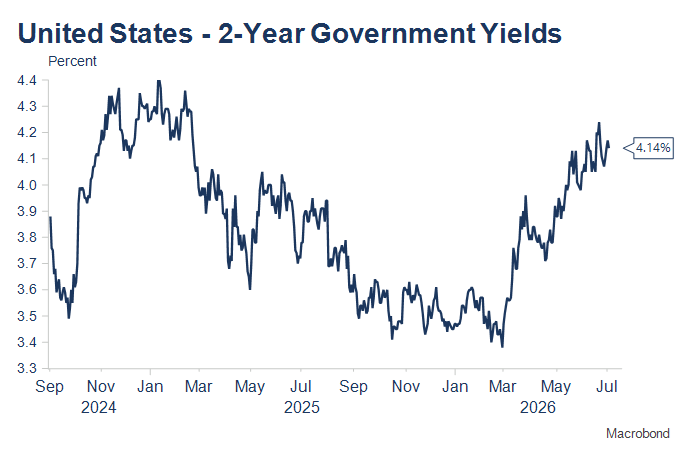

US 2-year, 10-year and Australian 10-year bond yields ended the week higher, even as oil prices continued to decline and non-farm payrolls printed weaker than expected. A stabilisation in technology stocks and the likelihood of somewhat tighter US monetary policy given continued above-target inflation likely explain these developments. US markets now almost fully price a rate rise by the late October meeting and have peak pricing of one and a half rate increases by the March and April meetings next year. The risk appears to be of an earlier move and still two moves, rather than one and a half.

In Australia, markets continue to signal reduced risk of any further move by the RBA, pricing just over a 50% chance of a move by the November meeting this year, with pricing thereafter “decaying” such that the market factors a 45% chance of an interest rate cut by the end of 2027. My core view is the RBA remains on hold in coming months, but that interest rates are still more likely to increase than decrease next, but perhaps not until late this year or early next year.