Perpetual Markets Economics and Interest Rate Commentary – 20 April 2026

Strait of Hormuz reopens then closes. Further peace talks expected this week. Speeches from RBA’s Hauser and US’s Williams last week important for monetary policy. Little in the way of data this week.

Key points

- Strait of Hormuz reopens for a few hours and then closes again on the weekend. Bonds and equities rally on the news while oil prices drop 10%, moves significantly reversed in weekend trading in IG Markets.

- The ceasefire is scheduled to end on Tuesday though JD Vance is heading to Pakistan for further peace talks today and Iran has not confirmed its attendance. There have been skirmishes in the Strait of Hormuz.

- How long the Strait of Hormuz remains closed is still key for oil prices, oil supply and medium-term inflation and activity impacts. Markets are largely priced for a relatively quick reopening.

- The Fed’s gave an excellent speech on Friday night entitled “One Transitory Shock After Another” while RBA Deputy Governor Hauser appeared in a Fireside Chat during the week. Both are well worth reading. Waller is still more inclined to cut interest rates reflecting his concerns about the US labour market, though conflict-related inflation may delay this a while. Hauser was not convinced Australian interest rates were yet high enough to return inflation to target but also noted that RBA staff were currently assessing whether the impact on activity of higher oil prices was likely to complement or replace further rate rises.

- Further appearances from Hunter and Hauser on Friday sounded like the RBA staff may present the case for a further tightening to the Board at the May Meeting, though that does not make this a done deal like the past.

- There is virtually no economic data of import to be released this week, nor Fed or RBA speeches. At times like this, the economic data is a long way behind the economy so the reports the RBA receives from its liaison contacts will be important. What I’m mostly hearing is that March data was relatively good, but that there have been more significant negative impacts on activity occurring in April. That makes sense as consumers and businesses take some time to respond to changes in economic circumstances. Significant weakness in Australian consumer and business confidence in March and early April is likely a sign of how things will develop unless there is a reasonably quick resolution to the crisis.

Middle East and market developments

The oil price dropped around 10% on Friday after Iran announced the Strait of Hormuz had reopened. In the event, the reopening proved very short lived, with Iran reclosing the Strait shortly afterwards after the US failed to remove its blockade. Reports of Iran firing on ships trying to leave the Strait and the US boarding an Iranian-flagged vessel attempting to breach the US’s blockade have seen oil prices rebound by 6.7% or US$5.50 in weekend trading on IG Markets. Still, the oil price has fallen a little over the week as markets remain hopeful that the warring parties will come to some agreement in the not-too-distant future.

Tuesday marks a key deadline with the US-Iran ceasefire scheduled to end. Further Pakistan-facilitated peace talks are reported to occur on Monday, with JD Vance again leading the US efforts. It was suggested last week the ceasefire might be extended a further two weeks to enable a more lasting peace agreement to be finalised.

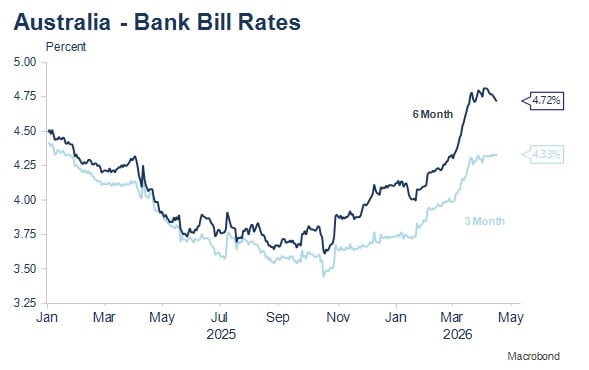

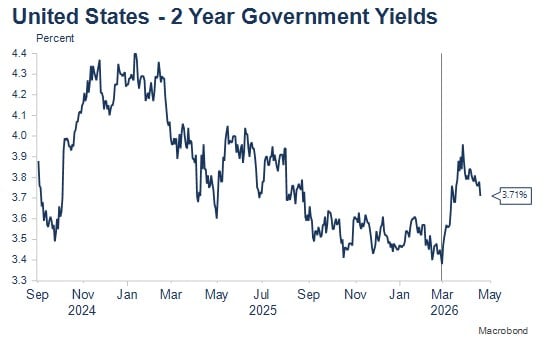

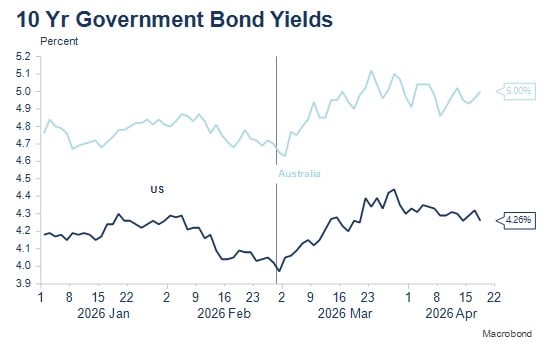

Short-term interest rates and longer-term bond yields were relatively quiet over the week, before dropping sharply on Friday on news of the reopening of the Strait of Hormuz. Some rebound is likely early on Monday given weekend developments. US markets continue to price some mild risk of a further US rate cut, though a full rate reduction is not priced until July 2027. Meanwhile, Australian shorter-term yields further discounted a third successive interest rate rise by the RBA, this now being 77% priced for May and 99% priced by June. I continue to think a June move is more likely.

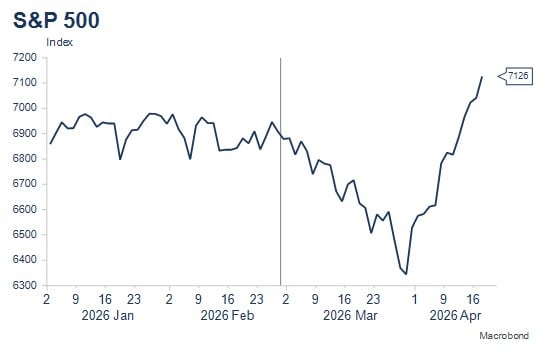

Equity markets continued their strong recovery, with the S&P 500 trading to new record highs in successive sessions over the week. The equity market appears the least affected by developments in the Middle East My assessment is the equity market is pricing a low probability that the Strait of Hormuz closure is an extended one and large benefits from the AI boom: over the near-term related to the data centre rollout, and over the longer-term for corporate profitability as costs are substantially reduced.

Central bank speeches last week and the outlook

There were two very interesting central bank appearances last week with important relevance to both the short- and medium-term course of US and Australian monetary policy. RBA Deputy Governor Andrew Hauser gave a Fireside Chat in New York, while Fed Governor gave a speech entitled “One Transitory Shock After Another”.

The structure of Waller’s speech accords quite closely with the approach to the Middle East conflict I have been writing about in recent weeks. Waller outlined the starting point economic conditions and then overlaid two scenarios related to how the Middle East conflict might play out.

Waller’s starting point included a relatively strong US economy, bolstered by business investment related to the AI boom, only slightly elevated inflation when the impact of tariffs is excluded, but a labour market, which despite being in balance as evidenced by the stable unemployment rate, had a fragile underpinning given both low hiring and low firing.

Various pieces of Fed research, to which Waller referred, have noted a significant reduction in net immigration – from around 2.3 million in 2024, to a negligible level in 2025 and so far in 2026. This means that with retirements related to the ageing population, virtually no payroll growth is consistent with stable unemployment. That said, Waller also noted that the duration of unemployment had been lengthening. This had led him to conclude in his previous speech in February that he was seeking greater clarity from the data as to whether he should vote for stable policy to make further progress towards 2% inflation or cut interest rates to support the Fed’s maximum employment goal.

Waller described two scenarios in relation to the Strait of Hormuz. The first is a relatively rapid reopening, which he thinks is a reasonable probability and which would mean that energy markets relatively quickly return to their pre-conflict levels without significant medium-term inflation or activity impacts. The second scenario is that of an extended closure of the Strait of Hormuz, which he described as a very possible scenario and one that is underpriced by the markets. This scenario could lead to energy prices bleeding into other prices and produce other supply chain constraints (eg fertiliser and helium affecting farm product prices) while broader energy supply shortages cause widespread production constraints.

This led Waller to conclude that the sequence of supply shocks currently hitting the US economy, could be like the sequence of supply shocks that impacted during the COVID pandemic and significantly increased US inflation and inflationary expectations. (I’m not as convinced by this argument as demand and labour market conditions during COVID were far stronger, though AI investment can provide a cushion for demand in this cycle). Waller’s sequence of shocks hypothesis produces two conflicting risks: on the one hand inflationary expectations could rise; on the other, the resulting reduction in activity could lead firms to tip from low firing mode into more significant labour market reductions.

The implication for Waller for US monetary policy was that an early reopening meant that he would continue to monitor the labour market for now but thought he was more inclined to vote for interest rate reductions in the medium term. An extended closure presented a more difficult balancing act, but one in which he either maintained current interest rate settings if he perceived inflation risks were higher than labour market risks or voted to cut rates if he perceived rising labour market risks.

Deputy Governor Hauser meanwhile described a five-point framework for thinking about the effect on the economy. Like Waller, the starting point was considered important and in Australia that included a tight labour market and inflation above target. Similarly, the size and duration of the shock was also relevant, which aligns with Waller’s quick reopening or extended closure scenarios. Hauser noted that there was not much the RBA could do to stop inflation rising in the short-term; obviously Australian monetary policy cannot reopen the Strait of Hormuz.

Hauser also noted that while the RBA did not want to see medium-term or long-term inflation expectations picking up, the RBA also needed to take account of the impact on activity from higher energy prices as this might help close the output gap (effectively reinforcing current monetary policy or substituting for additional policy tightening). I continue to be less convinced by the RBA’s output gap analysis and capacity constrained narrative and see current inflation as more reflective of labour market tightness. Nevertheless, the Deputy Governor suggested the former was the big question the bank’s staff were working on in relation to the May forecast update: what was the energy shock going to do to activity and inflation over the medium term?

In response to a question about whether interest rates were currently high enough, Hauser noted that interest rates would have to go to a level that would bring inflation back to target and that he did not have high confidence that interest rates were yet at that level.

This seems to suggest significant risk of a further interest rate rise in May, in fact in the absence of the Iran conflict, that’s probably what I would do to ensure inflation returned to the 2.5% target a little earlier than currently forecast in mid-2028. However, Hauser also added comments that cast a little doubt on the prospect of a May rise, noting that the bank would need to monitor the new shock closely. He also commented that if firms push price rises through, the RBA would respond, but that he didn’t know if they had seen enough yet to respond. Admittedly, this comment could be in relation to second round inflation effects, rather than a continued recalibration of policy to pre-Iran circumstances.

While I have become more hawkish on the need to reduce inflation as inflation has remained above target and the cumulative cost of living rise has become larger, at the current juncture, it would seem more prudent to me to wait until the course of the conflict becomes a little clearer. It wouldn’t make sense to tighten in May when an extended closure might mean the need to cut interest rates reasonably soon if global and Australian recession threatened.

That said, my key assessments and assumptions at this stage are:

- The conflict will soon end and the Strait of Hormuz reopen, removing the extended closure and recession scenario. The latter is reinstated in the case of an extended closure.

- The RBA will have to further tighten policy if this occurs – once to twice only should be priced in the near term, still in my opinion more likely in June than May, but likely not back-to-back at both meetings.

- The world economy will return to the pre-existing fundamentals of a recovering US economy, which should generally have a bearish tilt to US interest rates.

- Medium-term, questions about the US labour market because of AI developments remain, which could impart a bias to lower longer-term yields over the medium term.

Economic calendar – key Australian and US events this week

It’s a very quiet week data and speech wise, with no tier one Australian economic data, the Fed in blackout and no RBA speeches scheduled. The US releases March retail sales data on Tuesday, which will include energy impacts on spending, with ex-food and energy spending assessed closely for any early impacts on other spending. The highlight is probably the NZ Q1 CPI on Tuesday, which will also contain energy price impacts on headline inflation, with less impact likely on core.

Key upcoming events and data releases include:

- Tuesday 21 April: NZ CPI (Q1).

- Wednesday 29 April: Australian March and March quarter CPI; FOMC Meeting.

- Tuesday 5 May: RBA Board Meeting and May Statement on Monetary Policy.

Chart review