Key points

- The time the Strait of Hormuz is closed remains the most important consideration for inflation, economic activity, unemployment and monetary policy.

- A quick or near-term resolution would likely see much of recent market moves reverse, while a longer closure (e.g. three to six months) would likely cause a global recession. In both cases, however, the closure and its economic effects can ultimately end quickly, unlike other recessionary causes.

- Unsurprisingly March ISM reports showed softer employment and higher prices, but in both cases, activity readings showed the US economy was strengthening ahead of the conflict. That’s an important consideration if the conflict ends soon.

- On that front, recent news has Iran rejecting a 45-day ceasefire proposal, arguing instead for a permanent end to hostilities, under certain circumstances. That seems favourable but comes as President Trump threatens a US 8PM Tuesday deadline for the reopening of the Strait of Hormuz or else attacks against Iran’s power infrastructure will begin.

- Later in the week, important updates on US inflation are published: the February PCE on Thursday and the March CPI on Friday. Both appeared to be running too hot even before the Iran conflict to permit any consideration of further easing in US monetary policy at present, with a tilt toward pricing tightening more likely based on pre-Iran developments.

- Markets have been a little more settled over the past week. Share markets improved sharply on earlier suggestions the war might end soon and have sustained this move even as oil prices reversed earlier declines. The Fed and RBNZ have signalled a period of observation on the economy and consideration of the medium-term impacts on inflation is warranted. That seems a prudent course of action given the unknown duration of the conflict and the lags with which monetary policy affects the economy. That’s what I would do at the May Board meeting if I was the RBA Monetary Policy Board, having recently tightened policy twice. Markets are only 64% priced for a follow up interest rate rise in May and almost but not completely priced for a further rise in June.

Data watch

As the calendar has ticked over into April, we’ll start to receive March economic statistics, which will provide some indication of the initial impact of the sharp rise in energy prices on the Australian and US economies. The data will provide only a partial indication, however, given some surveys occur early in the month, oil prices rose throughout the month, and consumers and businesses usually take time to adjust to changes in economic circumstances.

That said, petrol and diesel prices have risen very sharply, in Australia reportedly also reflecting much stronger demand, fuel and transport surcharges have appeared very quickly with major supermarket chains warning of imminent broader price rises and there has also been very rapid pass through of price rises into some building materials prices, with a 36% increase in PVC pipes receiving much coverage in the Australian press. The latter reflects supply chain disruptions in the Strait of Hormuz.

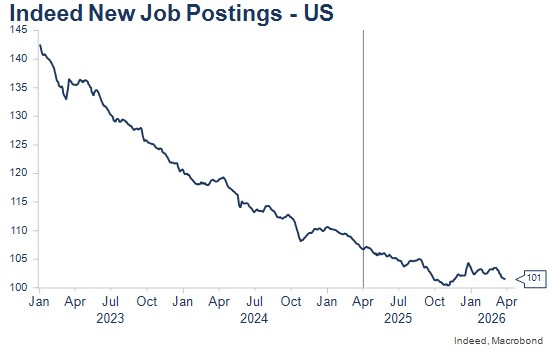

Long-term readers will know I am a big fan of labour market indicators and in particular job advertisements in Australia, with March data to be published by ANZ Indeed today. I have also been following Indeed’s daily job postings’ series in the US since the Liberation Day tariffs were announced last April to monitor for any sharp deterioration in the US labour market. The chart shows there was only a mild easing in demand due to the tariffs but that US firms have reacted quickly to the sharp rise in energy prices since the start of March. Job postings have fallen around 3% over the month. This will be an important indicator to follow in coming days and months.

Economic scenarios

It’s not possible for economists to forecast how the economy and monetary policy will ultimately turn out with any degree of certainty at the present time, because so much depends on the course and length of the military conflict. As I have been writing in recent weeks, the time the Strait of Hormuz is closed likely remains the number one determinant of the oil price and the course of global economies and inflation, while damage to energy infrastructure in the region is likely the second most important consideration. Both depend on how soon the warring parties resolve their differences and when Iran will allow vessels of other nations shipping access to the Strait of Hormuz. At this stage, the Strait remains effectively closed.

There appear to be two bookend scenarios, with a range of various alternatives in between:

- A quick resolution to hostilities and reopening of the Strait of Hormuz. This should see supplies of energy and other related products such as fertiliser and plastics begin to flow relatively quickly, reversing much – but probably not all – of the current sharp price rises in the near term. This would see the economic outlook mostly return to that which existed prior to the conflict, which was mostly characterised by an improving outlook for the US and world economies as the AI investment boom rolled on.

- An extended closure of the Strait of Hormuz (e.g. three to six months or longer). This would likely result in much higher oil prices than have been witnessed to date, producing much higher inflation and cost pressures throughout global economies. In turn, this would likely cause a global recession, with consumers’ budgets squeezed and firms cutting back output and employment.

Looking at the current oil price, it would seem that markets are only pricing around a 10-15% chance of the second, extended closure scenario at this stage, as this would likely produce spot oil prices in excess of US$150pb, or even higher, being the price required to destroy 20% of global oil demand in the short term. That said, it’s also important to remember that even an extended closure could ultimately end quite quickly, reversing much of the negative effects on growth and inflation.

How might central banks react to this energy price shock?

Pronouncements from many central banks since the crisis broadly agree that monetary policy should look through the first-round effects on inflation of oil price rises but be concerned about the medium-term impact on inflation and on inflationary expectations and pricing behaviour.

This saw RBNZ Governor Breman noting that the RBNZ will spend some time (perhaps months) assessing the impact of the crisis on medium-term inflation, while Fed Chair Powell noted that US monetary policy was well-placed for the FOMC to spend some time assessing the impact of the crisis on the Fed’s dual mandate of full employment and 2% PCE inflation. Powell also commented that the context was important, with inflation having been above target for an extended period before the recent spike in oil prices, suggesting any early resumption of easing is unlikely without significant impacts on unemployment. US markets now price no further easing before the end of the year, with a tilt toward tightening pricing likely.

Powell’s press conference also noted that this was the third successive supply shock to hit the US economy in short succession: COVID, tariffs and now Iran. Monetary policy is much better suited to dealing with demand shocks, as the impacts on the Fed’s two goals, inflation and employment, are not in tension. The latest supply shock – if sustained - will raise both inflation (suggesting tighter policy) and unemployment (suggesting easier monetary policy).

During the tariff supply shock, the Fed provided the analytical construct that monetary policy should look at both the size of the deviation of the policy goal from target, but also the length of time that the policy goal was expected to remain away from target.

If applied to the COVID supply shock, the monetary policy implications were very clear as unemployment was very low, and inflation was diverging sharply from target. During the tariff shock, while inflation was expected to rise and unemployment remained low, a period of stable (or potentially higher) interest rates was reasonable. In the event, of course, the inflation outcomes from tariffs beyond the first-round effect, were much less than expected. Excluding tariffs, inflation was assessed to be running close to target. This allowed the Fed to reduce interest rates in late 2025 as concerns grew about downside risks to employment.

How might the current situation play out? To repeat myself, much depends on how quickly the conflict resolves. Monetary policy acts with long and variable lags, so tightening aggressively now, when the conflict might end in a few weeks, would not be a reasonable course of action, though of course a central bank could also decide to quickly reverse that decision.

In an uncertain time, there is always value in awaiting more information rather than making a decision that may quickly turn out to be wrong. Four RBA Board members voted to follow this course at the March Board meeting, even though they considered further near-term tightening of policy was likely. The starting point for monetary policy is also important – if monetary policy was already clearly expansionary, a central bank might wish to move policy to a less expansionary setting heading into a known inflationary shock.

What we know about the current situation is that its duration is very unknown, it is already having significant inflationary impacts – and I would argue very quick flow on pricing as transport costs are passed on - and it is likely to have negative impacts on activity and employment. Tightening monetary policy now could assist in reducing the likely second-round impacts of inflation, but only at the cost of even higher unemployment, which is likely to rise in the months ahead if oil prices remain elevated. For now, if I was the RBA (and as the Fed seems to be doing), I’d await further information on the correct policy response until the June Board meeting, having recently tightened twice and moved policy closer to a restrictive setting. The message accompanying a May hold would be very hawkish, with the likelihood that some further tightening (one to two more interest rate rises) will be required to dampen inflation pressures.

Stagflation

I wrote a little about stagflation last week, noting that the term has been used mainly incorrectly in recent years. Stagflation was the period during the early to mid-1970s when the world experienced simultaneous and sustained very high inflation and very high unemployment. Recent years have had temporarily higher inflation (not very high inflation) but low unemployment.

Energy supply shocks are always stagflationary in nature, acting to simultaneously increase inflation and unemployment. The extent to which the situation is sustained will depend first on the length of military hostilities and second on the policy response. Monetary policy tends to be best at dealing with demand driven inflation, while fiscal policy can react to all natures of unemployment sources. If a true stagflationary environment was to arrive, it would be likely that the two arms of policy would need to focus on the aspect of the policy challenge they are best suited to – monetary policy on controlling inflation and fiscal policy on supporting the unemployed and small business.

Economic Calendar – key Australian and US events this week

Monday 6 April – Non-manufacturing ISM (the employment question will be very important to follow in coming months, with the March reading showing an immediate impact on firms’ employment intentions and a sharp jump in price pressures).

Tuesday 7 April – Household Spending Indicator (February); ANZ Indeed Job Ads (March); Melbourne Institute Inflation Gauge (March). (Overnight) the Fed’s Goolsbee on Monetary Policy. The Melbourne Institute series will be worth a look to see how quickly inflation has picked up beyond fuel (probably more noticeable in April), while job ads might show an initial impact on labour demand. Household spending is expected to rise 0.2-0.3% m/m, a little more subdued than in recent months, but of course this pre-dates the rise in energy prices through March.

Wednesday 8 April – RBNZ Governor Breman indicated last week that the RBNZ would only react to developments that affected inflationary outcomes over the medium term and furthermore suggested that this might take some months to ascertain. That suggests it’s very unlikely there will be any change to NZ monetary policy at this meeting, though it would not be surprising to see more hawkish commentary as the risks to inflation and inflationary expectations have tilted sharply to the upside, though risks to activity and unemployment have tilted to the downside. (Overnight) the Fed’s Jefferson on The Economic Outlook and the Fed’s Daly makes keynote remarks.

Thursday 9 April – (Overnight) US PCE deflator (February). This data of course also pre-dates the sharp escalation in energy prices in March. Nevertheless, market forecasts are for the second consecutive 0.4% m/m increase, a rate that is clearly inconsistent with the Fed’s medium-term 2% PCE target and should not see US markets discounting any near-term easing and more likely build in some tightening pricing.

Friday 10 April – (Overnight) US CPI March. A 0.3% m/m and 2.7% y/y ex food and energy reading is expected. There will also be considerable interest in the extent to which the University of Michigan’s long-term (5-10 year) inflationary expectations series moves. Markets are expecting a lift from 3.2% to 3.5%. The Fed (and other central banks) will be sensitive to any rise in longer-term inflationary expectations.

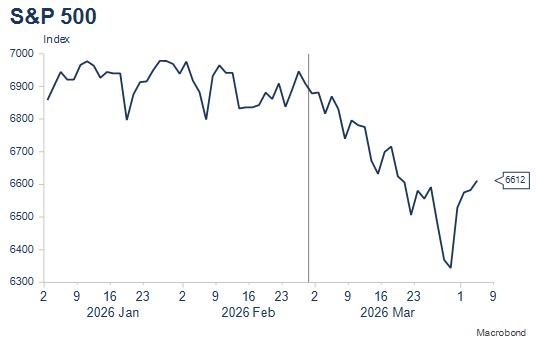

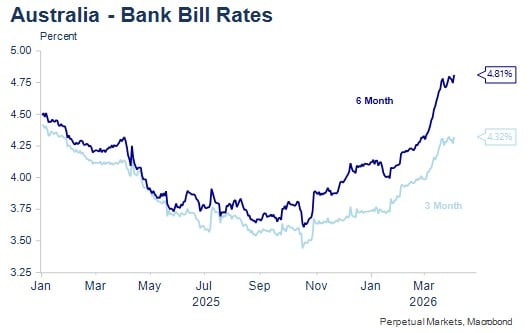

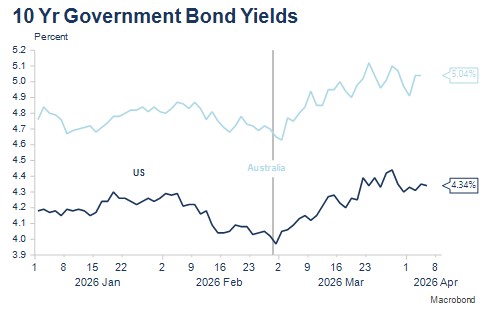

Chart Round-Up