Perpetual Economic and Interest Rate Outlook – 2 March 2026

Operation Epic Fury, Month in review: strong Australian data while markets worry about AI effects, key events in Australia and the US this week

Key Points

- More recent Middle East conflicts involving the US have tended to be relatively short-lived reflecting very dominant weaponry. This has reduced the impact on markets more broadly than the initial oil price spikes.

- That’s not to say this is how this situation will ultimately turn out. The key issues are the extent to which oil prices rise, particularly how long they stay elevated and the extent to which oil infrastructure is damaged. US and Israeli strikes to date appear quite targeted.

- The operation began after markets closed on Friday. IG Markets weekend markets show stocks down around 0.75%, oil up over 11%, gold up nearly 3% and silver nearly 5%, while the US$ had weakened a little against the EUR and JPY. Early moves on Monday are broadly similar, though rises in oil prices and precious metals have been pared. Australian interest rate markets have rallied as markets expect the uncertainty to cause the RBA to push back the timing of any further interest rate tightening.

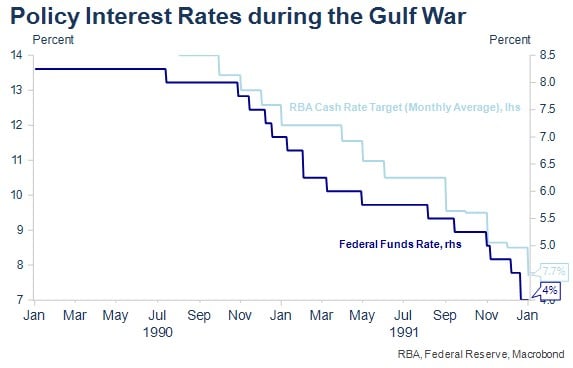

- The Gulf War saw the US Federal Reserve and RBA focusing on domestic economic fundamentals and continuing to ease as both economies entered recession, which the oil price accentuated but did not cause.

- The current uncertainty and tightening in financial conditions will likely see the RBA Board choose to wait at least until the May Board meeting before tightening further, a delay which it seems to have been signalling. This major geopolitical development among other very large structural changes again reinforces how futile the central bank’s reliance on modelling currently is. Good judgement is needed now more than ever.

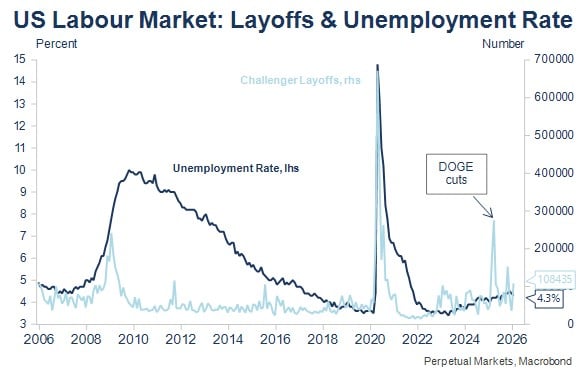

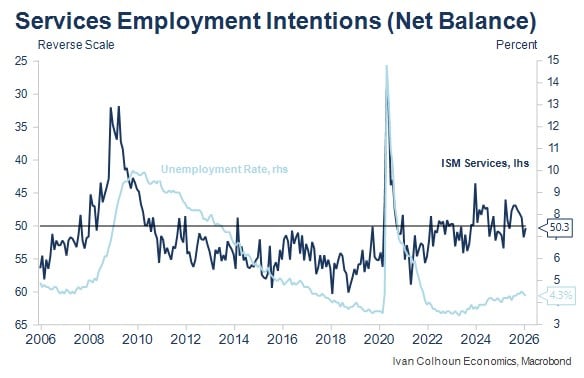

- Military-related market developments will likely predominate this week, though US labour market and ISM survey data are important after surprising strength in each indicator last month. The ISM Services employment question is currently the most important indicator I’m following each month, along with Indeed job postings in the US.

- I continue to closely monitor the thoughts of Governor Waller, who was early in detecting weakness in the US labour market last year and in arguing for further easing. Unless labour market data at the end of the week are strong, he favours further easing. His recent speech on this topic is worth a read: Speech by Governor Waller on the economic outlook.

- More broadly, the longer-term impact, of AI on employment remains the biggest macro and interest rate question of all, though the short-term may also present some capacity pressures on electricity, water and semi-conductors given the size of the global data centre rollout. Longer-term, bond markets appear to have caught a bid and AI-related job losses seem to be driving these concerns. Credit markets are also dealing with the very swift and large repricing of a number of major Software names.

Operation Epic Fury

While it’s a huge week ahead for data in both Australia and the US, developments in the US/Israel conflict with Iran will be most likely to significantly shape markets this week. That said, last week still saw a significant under-current of longer-term concerns about the impact of AI on employment that appears to be supporting US and Australian bond prices (lowering yields), while selected tech stock prices continue to fall. The size and sharpness of the fall is also causing some issues in private equity and credit markets.

US and Israeli forces commenced Operation Epic Fury on Saturday in the region. The US targeted the Iranian leadership, while Israeli forces targeted Iran’s ballistic missile sites. Both the US and Iranian media confirmed that Iran’s Supreme Leader, Ayatollah Ali Khamenei had been killed in the strikes, along with other senior leaders of the regime.

Markets had closed for the week, when the operation began, though IG Markets has several weekend markets, which reveal unsurprising directional moves (oil up over 11%; Gold up around 3%, Silver 4%, US equities -0.75% and US$/JPY -0.2%).

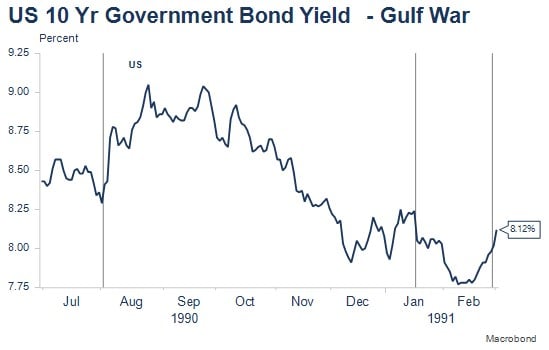

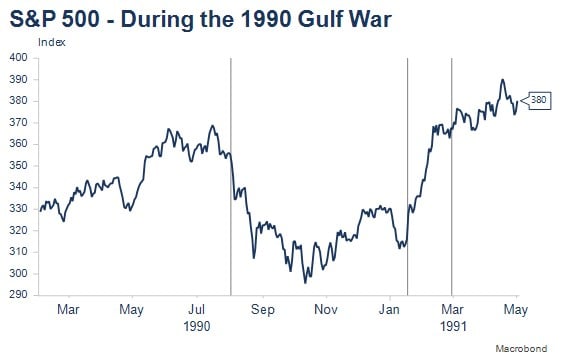

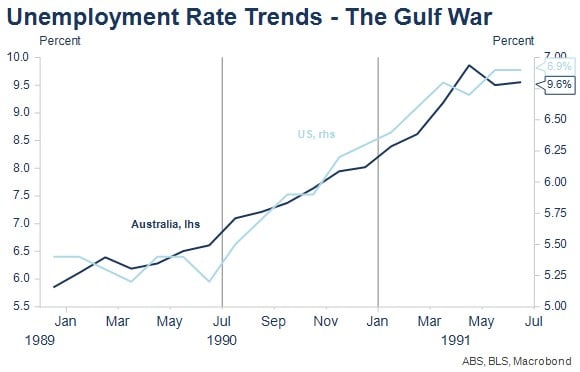

We can consider the implications for markets and economies by looking at previous US military operations in the Middle East and by outlining some key aspects for consideration. Looking at the original Gulf War in 1990/1991 (operations Desert Shield and Desert Storm), we learnt that oil prices rose significantly initially, bond yields on that occasion rose on inflationary concerns, while stocks weakened.

The broader economic context was important in terms of the reaction of both policy interest rates, equities and currency developments. Both the US and Australia were entering recession, not caused by the Gulf War, but exacerbated by the higher oil prices and bond yields that resulted for a time. Importantly, while war uncertainties may have delayed easing moves in the US a little, in the end, both central banks reacted to the domestic economic fundamentals they faced and continued to reduce interest rates as unemployment rose in both countries.

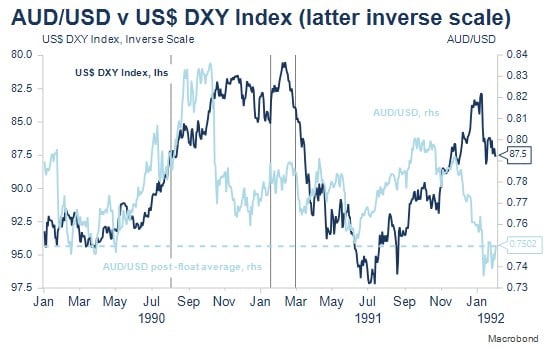

The US$ was weakening sharply as the Gulf War began, which along with the resultant higher energy prices and favourable interest rate differentials with the US, saw the $A continue to rise. A sharp fall occurred in October 1990 as it became apparent the $A’s valuation was not justified based on rapidly deteriorating economic fundamentals.

Importantly, much of the military-related pricing moves had reversed or were in the process of reversing ahead of Operation Desert Storm, though in part this reflected global recession. It was true that once Desert Storm got underway, the superiority of the US and its allies saw markets generally unwind remaining existing war premia or discounts.

More recent conflicts have shown similar initial spikes in oil prices but often the spikes have been smaller, less sustained and the flow-on implications to other markets reduced such has been the military superiority of the US and allies. In general, it’s important to consider both the extent of the rise in the price of oil, the length of time the price spends elevated and monitor oil infrastructure damage that could affect global supplies. The importance of the countries in question as oil producers (Iran produces around 3-4% of global oil) and the underlying global economic context are also important e.g. AI developments won’t be significantly affected by the conflict.

In the short term, the dominance of the US military (or otherwise) is likely to be the key consideration. To the extent the US military action is very successful, the impact on markets is likely to be reduced and/or short-lived. I’m not a military strategist, however, I’d make the observation that except for Russia and Ukraine, where the US has not become involved, this has generally been the playbook of recent conflicts. That would be my base case.

Month in Review

While February was a short month, there were still very significant economic and market developments, with two of the Megatrends previously written about to the fore, namely AI and geopolitics. The following key events and market movements occurred:

- The RBA’s Monetary Policy Board raised the official cash rate by 0.25% to 3.85% as RBA staff could not forecast the return of inflation to target in a reasonable timeframe without policy action, given developments in inflation, demand and unemployment. The updated forecasts assume a further interest rate increase this year, and even then, inflation only returns to around 2.5% in mid-2027, arguably stretching the definition of “in a reasonable timeframe” given the extended period of above-target inflation already experienced.

- Subsequent communications from RBA staff attributed the about face on interest rates to three factors: 1) a stronger than anticipated world economy (due to AI spending and lesser than expected tariff effects – this is reasonable); 2) financial conditions were less restrictive than perceived (this seems a less reasonable argument); and 3) the Australian economy has greater capacity constraints than previously assessed (this seems unreasonable and involves a certain amount of back-fitting longer-term economic developments and explanations to short-term inflation outcomes). Importantly, the RBA staff is guiding the Board that much, but not all the recent higher inflation outcomes are likely to be temporary.

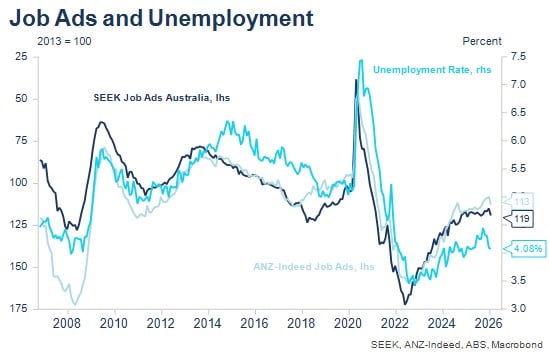

- Important Australian economic data showed unemployment remaining at a tighter than full-employment rate of 4.1% in January, while January trimmed mean inflation of 0.316% m/m was again faster than consistent with the midpoint of the RBA’s 2-3% target band.

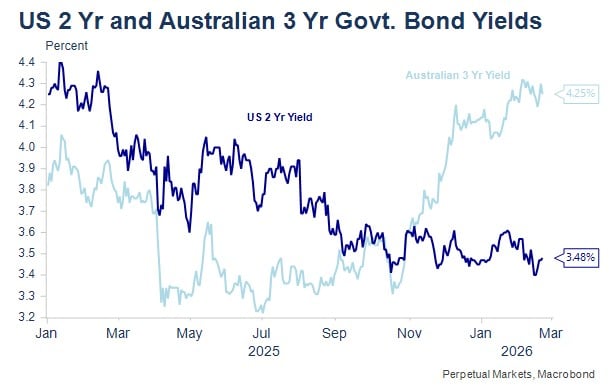

- US stock and bond markets were again relatively volatile, reflecting the market pricing the likely impact of AI on employment and business models of certain firms over the long-term. Software as a service companies’ share prices were particularly hard hit and a number of these companies have already announced hiring freezes or significant layoffs. Overall US ten-year bond yields ended the month 29bps lower, while the US market is now pricing three interest rate cuts by mid-2027. It seems that the longer end of the bond market is currently prepared to look well ahead for the impact of AI on employment. What happens directionally in US bonds, usually is reflected in Australian bond yields too. The Australian 10-year bond yield dropped 15bps over February and fell a further 8bps on the open today.

- After talks between the US and Iran throughout February, US and Israeli forces commenced Operation Epic Fury in late February., with initial significant impacts on oil and precious metal prices, but less of an impact on share prices. Other relevant market developments include the substantial but not full recovery of precious metal and copper prices from January’s swoon.

Economic Calendar – Key Australian and US events this week

- Monday 2 March – ANZ Job Ads (February), Melbourne Institute Inflation Gauge (February), Company profits (Q3), Inventories (Q3), RBA Hunter Remarks; (overnight) ISM Manufacturing (February).

- Tuesday 3 March – RBA Bullock Speech; $300m 2047 Bond Tender; Building Approvals (January); Net Exports/BoP (Q4); Government Spending (Q4).

- Wednesday 4 March – GDP (Q4); $900m 4.75% 2037 Bond Tender; (overnight) Services ISM (February); Fed Beige Book; ADP (February).

- Thursday 5 March – Household Spending Indicator (January); (overnight) Challenger Layoffs (February).

- Friday 6 March - $800m 1.5% 2031 Bond Tender; (overnight) Non-Farm Payrolls (February); US Retail Sales (February).

- Saturday 7 March – RBA Deputy Governor Hauser remarks (New York).

- Speeches from the Fed’s Williams and Kashkari (Tuesday), Daly and Paulson panel appearance (Thursday), Hammack (Friday). Communications blackout period begins 8 March.

If we abstract from the US and Israeli military operation for a while, this week sees a raft of important US data released. While Australia releases Q4 GDP, I consider this a very dated statistic and do not spend too much time analysing it. For the record, the market and the RBA are forecasting a 0.7% q/q increase and 2.2% y/y outcome. Speeches from RBA Assistant Governor Hunter on Monday evening and Governor Bullock on Tuesday, along with ANZ Job Ads and the Melbourne Institute’s Inflation Gauge on Monday, will likely be the Australian data highlights of the week.

I’m also expecting another weakish consumer spending reading as the payback from strong October and November Black Friday sales completes (the market is expecting +0.4% m/m). Job ads jumped sharply in January (+4.4% m/m) but are at risk of dropping commensurately in February, given difficult to adjust large seasonal variations at this time of year, while trimmed mean inflation expectations were low in December after two strong months. The extent of bounce back in February is important.

US data will likely prove far more interesting, especially, various US labour market updates, as markets continue to grapple with the ultimate extent of job shedding due to the introduction of AI. For me the latter remains the most important macro question of all over the medium term, with a short-term issue as to the extent to which resources such as semiconductors, water, copper and electricity could face shortages. On Monday and Wednesday there’s also the ISM surveys for Manufacturing and Services, both of which surprised on the strong side in January (as did employment). The ISM services employment question remains key, but the markets seem to be running a long way ahead of labour market data at present – and are likely to continue to do so. Have a read of the Waller speech in the introductory dot points.