US CPI, NAB Business Survey and lots of Fed speakers the highlights. US interest rate pricing continues to slowly shift bearishly.

Key points

- After a few weeks with very little Fed communications, at least nine FOMC members are speaking on the economy this week, while Chair Warsh testifies before both House and Senate committees. The Fed also releases the Beige Book for the July 28-29 Meeting before going into blackout next weekend.

- I’m following closely the emerging debate about AI-related inflationary pressures, which NY Fed President Williams noted last week was his top inflationary concern. Former RBA Deputy Governor Guy Debelle noted in a recent paper that the US AI investment boom is similar in proportion to Australia’s very large (and inflationary) mining boom of the early 2000s. Debelle notes energy prices are one of the three prices that will shape the next phase of Australia’s economy.

- That AI boom is behind my view that Australia and the US will both experience elongated tightening cycles as often occurs in investment booms. I continue to look for two interest rate rises by the Fed before the end of the year but see the RBA on hold in the near term before eventually slowly tightening further.

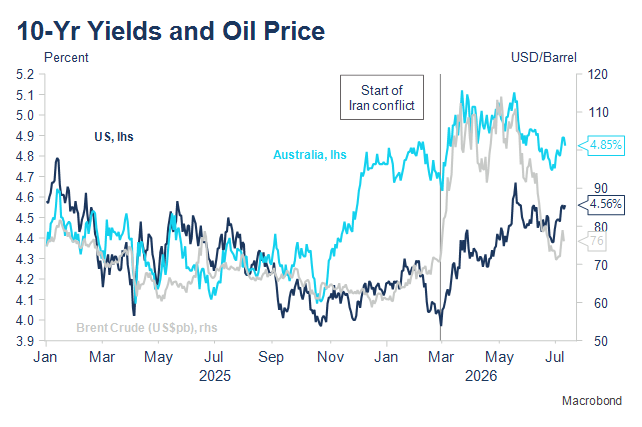

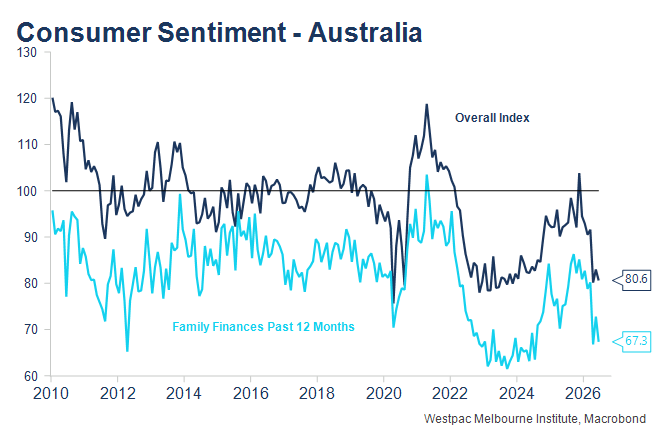

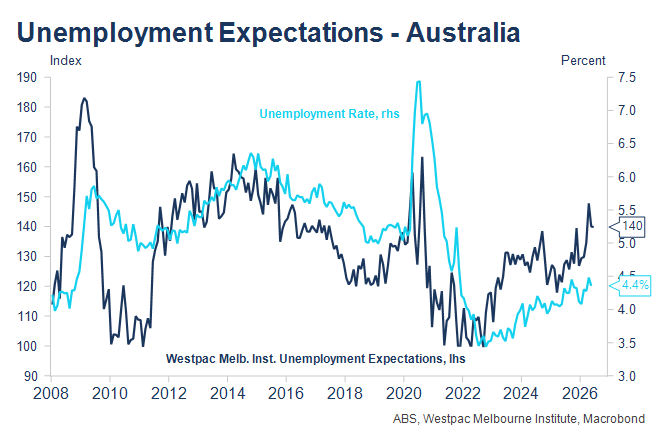

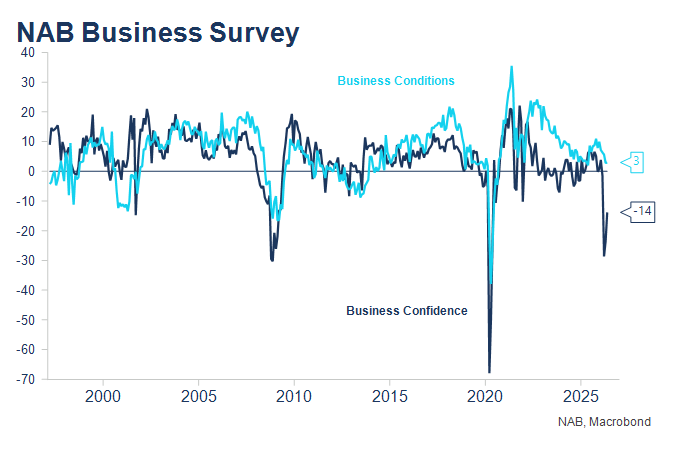

- This week the key Australian releases are on Tuesday. I’ll be analysing Consumer Confidence and the NAB Business Survey from the perspective of trying to ascertain how much of the recent softness reflects oil prices compared to higher interest rates. My prior is that more relates to oil price effects. I’m expecting improvements in both series to be recorded this month, reflecting lower oil and diesel prices, and would be surprised if NAB’s capacity utilisation measure did not tick higher.

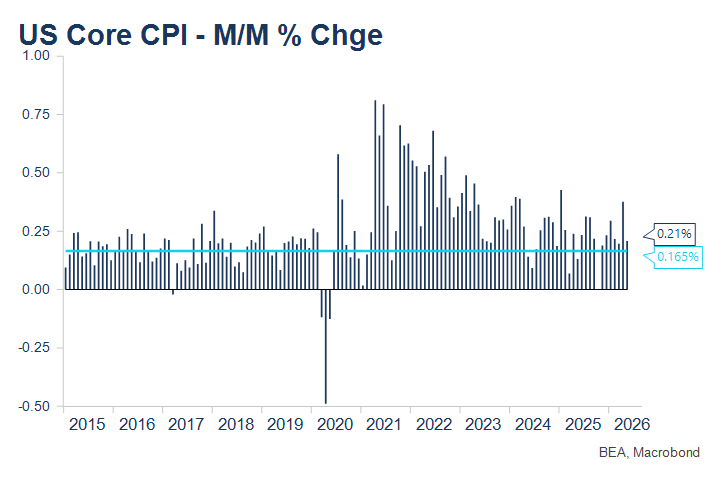

- In the US, there are two key releases: the US CPI on Tuesday, where a just acceptable 0.2% m/m core rate of inflation is expected and Retail Sales, where the market expects the control figure to record a 0.5% m/m gain after last month’s relatively strong 0.7% outcome. In both cases, nominal retail spending might reflect indirect energy impacts.

The week ahead – lots of Fed speakers, the NAB Business Survey and US CPI

All times shown are AEST.

Tuesday 14 July

- 02:30am Waller Speech

- 10:30am Westpac Consumer Sentiment, July

- 11:30am NAB Business Survey, July

- 10:30pm AEST US CPI (June)

- Midnight: Fed Chair Warsh House Testimony

Wednesday 15 July

- 02:40am Barr Speech on AI

- 03:00am Goolsbee Fireside Chat

- 03:30am Cook Speech

- 04:55am Bowman Speech

- 10:45pm Williams Keynote Remarks

- Midnight: Fed Chair Warsh Senate Testimony

Thursday 16 July

- 3:00am Cook Speech on the Economic Outlook

- 4:00am Beige Book

- 10:30pm US Retail Sales (June)

Friday 17 July

- 02:30am Logan Speech on the Economy and Monetary Policy

- 03:25am Schmid Speech

- 09:00am Jefferson Speech on the Economy and Monetary Policy

- Midnight: US University of Michigan Consumer Sentiment and 1-Yr and 5-10 Yr Inflationary Expectations

- Midnight: Fed’s External Communications Blackout begins

Since Chair Warsh’s first FOMC Meeting and Press Conference, there have been far fewer speeches given by Fed officials, in a taste of what’s likely to be more the norm after the Task Force on Communications reports later this year. This week’s calendar is more like the pre-Warsh Fed, with speeches from around nine separate officials and appearances before House and Senate committees by Chair Warsh. The Fed also releases the Beige Book relevant to the July 28-29 FOMC Meeting.

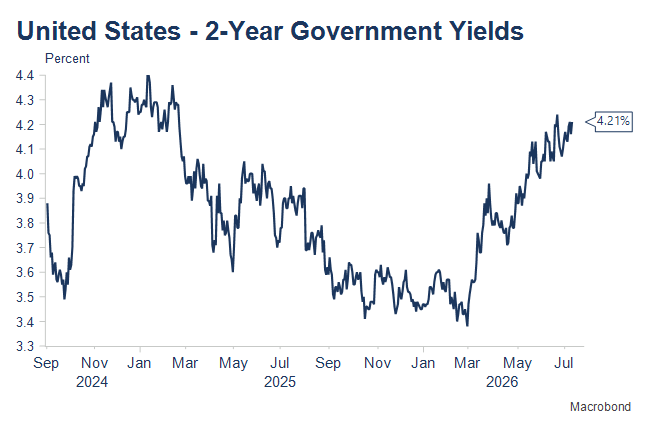

The content of speeches will likely provide a further update on how various participants are shifting their views on inflationary and labour market risks. We learned in the relatively hawkish June FOMC Minutes last week that inflationary risks had risen, while downside risks to unemployment had reduced “a bit”. US interest rate pricing shifted bearishly over the week, such that now a rate rise in more than fully priced by the late October meeting, one and a half rate rises are priced by year end and nearly two full increases are priced by the 28 April meeting in 2027. Last week, only one and a half rate increases were priced by that April meeting.

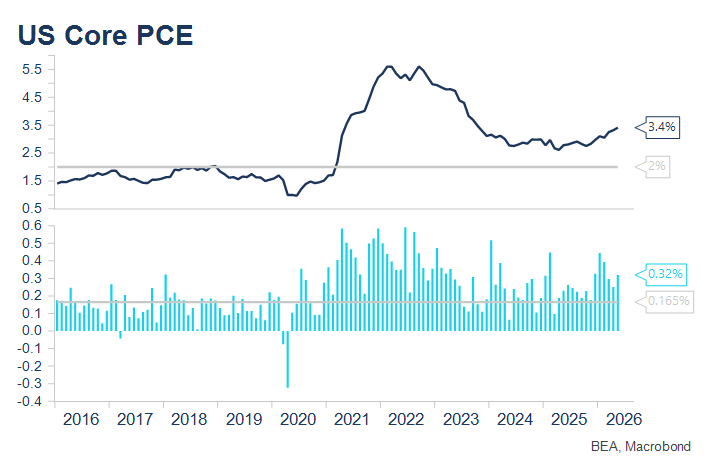

Bearish US interest rate developments over the past week included: the hawkish Fed Minutes, President Trump declaring the end to the ceasefire with Iran, which produced somewhat higher oil prices, and for me, most interestingly reports of comments from NY Fed President Williams: Fed’s Williams Says AI Is Now His Main Inflation Concern. Williams noted that AI-driven inflation was now his top inflation concern and was reported to have argued that monetary policy would have to be tightened if core PCE continued to run above 0.2% m/m in the second half of the year. Former RBA Deputy Governor Guy Debelle also penned a piece for the e61 Institute, where he noted the AI investment boom in the US is equivalent in size to Australia’s mining investment boom of the early 2000s, but for an economy ten times the size of Australia: The three prices that will shape the next phase of the Australian economy – e61 INSTITUTE.

My base case remains that a moderation in oil prices will allow the AI investment boom to shine through as the dominant force for activity and inflation, particularly in the US, but also in other countries around the world as data centres are rolled out and demand is strong for copper, semi-conductors, energy and water. This is expected to see the emergence of elongated tightening cycles in both countries, but more so in the US.

The key US data print this week is the June CPI. The core CPI is forecast at 0.2% m/m and 2.9% y/y, identical rates to May. Core PCE has been running faster than the CPI, so a high 0.2% or a 0.3% outcome would reinforce the need for the Fed to tighten interest rates modestly in the second half of this year. I continue to look for two rate rises this half, with the first increase to occur earlier than the October meeting currently discounted.

In Australia, we receive the latest updates on consumer sentiment and on business confidence and conditions. Business conditions, cost and price measures, capacity utilisation, and unemployment expectations are the four important series to follow from these releases. It would not surprise to see some improvement in consumer sentiment given the recent falls in oil prices. Energy prices – and more broadly, the cost of living – have been an important factor in the continuing low level of consumer confidence. The unemployment expectations series has from time to time provided a useful lead on unemployment trends. Again, it wouldn’t surprise if some of the significant deterioration that occurred in the wake of the commencement of the Iran conflict unwound. The unemployment expectations signal should be monitored for confirmation or rejection of the slight deteriorating trend for SEEK job ads in recent months.

The NAB Business Survey is a more important indicator than Consumer Sentiment. The extent to which business conditions recover, stabilise or continue to deteriorate in coming months, as oil prices normalise, will provide an indication of the extent to which oil prices or interest rate rises were responsible for the recent deterioration in conditions. My prior is that more of the recent weakness reflected higher energy prices than higher interest rates.

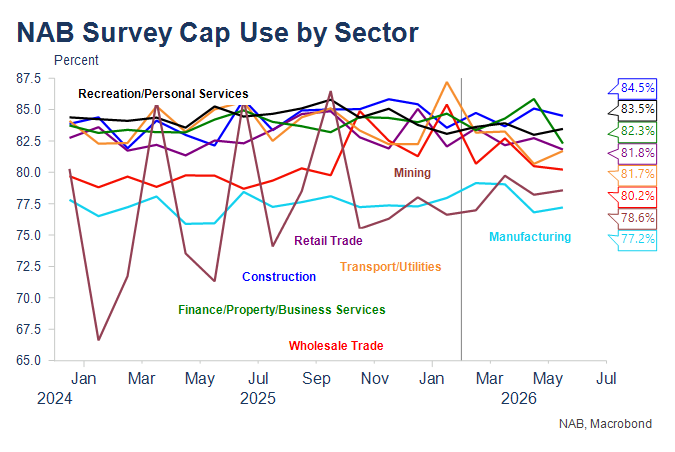

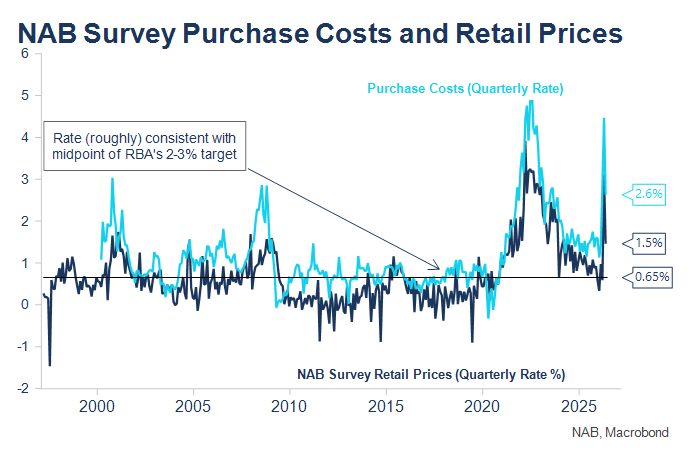

Interestingly, in the Services ISM released last week, where I was looking for an earlier improvement in prices than recovery in employment, the reverse occurred. In June, I’m expecting to see a further improvement in business confidence and conditions, further reduced rates of cost and price increases, and an improvement in capacity utilisation (both may be more evident in the July survey). The latter has become an indicator that has been more focused on given the RBA’s narrative about the Australian economy being capacity constrained, though there seems little evidence of capacity constraints beyond the labour market and housing market.

The reduction in capacity utilisation in recent months has been broad-based, though interestingly not in Construction and less surprisingly, also not in Mining, both sectors benefiting from the AI investment boom.

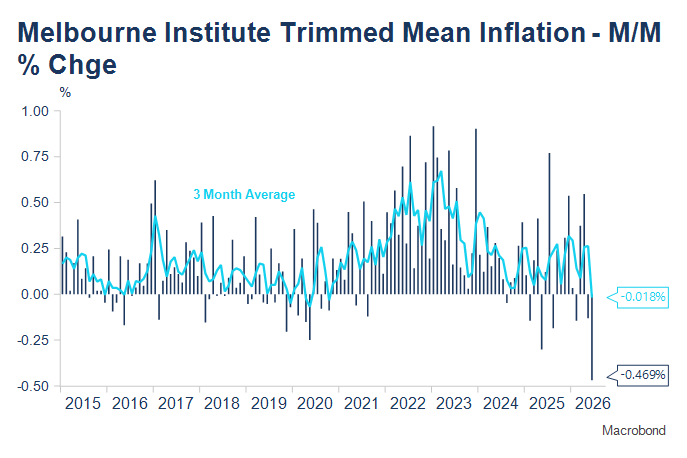

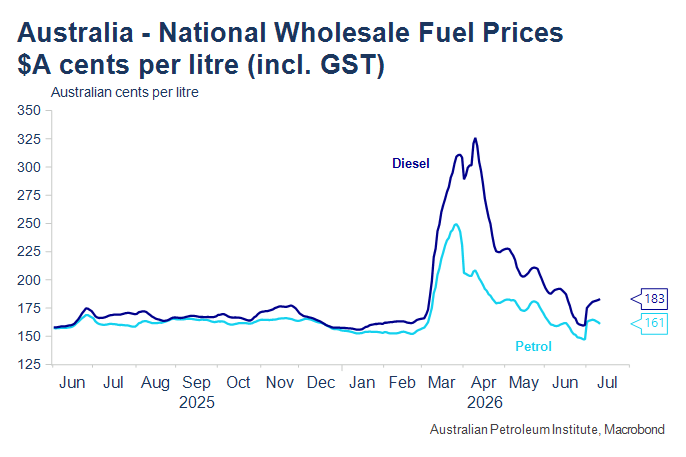

Importantly, the Melbourne Institute Inflation Gauge released last week showed the largest monthly decline in over ten years, suggesting both a pullback in the NAB Survey measures, and downside risk to the RBA’s May SMP 1% Q2 trimmed mean forecast. Monthly CPIs in April and May suggest a 0.8%/0.9% outcome is still too high on a sustained basis for at-target inflation to be achieved. Falling house prices raise the possibility of some renewed discounting of newly constructed dwellings, while petrol and diesel prices are back closer to pre-conflict levels, though both prices still include around 16 cents per litre of government subsidies that are due to end at the end of this month.

Australian and US interest rate market developments

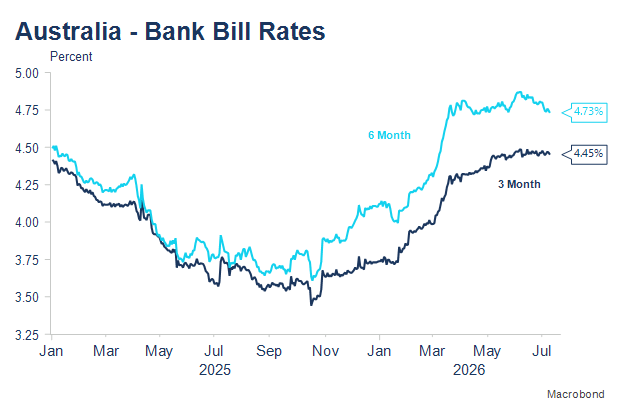

US interest rates sold off across the rate spectrum as the market continued to reprice the risk of Fed interest rate rises over the coming year. While the market is now getting close to pricing the two nearer-term interest rate rises I expect that pricing still needs to shift earlier in my view. The resultant sell-off in longer-end US yields dragged Australian longer-dated yields higher also, though the shorter-end of the Australian yield curve was relatively anchored as the market continues to attach only around a 50% probability of a further interest rate rise from the RBA by the end of the year. That dynamic where US longer-dated yields drag Australian long yields higher could be an extended trend if construction-related AI investment continues to create inflationary pressures.

The pricing of the next move in Australian interest rates being a cut has reduced over the past week, most likely reflecting the sell-off in US interest rates rather than any significant reappraisal of the Australian interest rate outlook. An increase at the August Board Meeting is now only 18% priced. My expectation remains that the RBA is likely to remain on hold for a number of months – ie not move in August, though a quarterly trimmed mean in excess of 1% q/q would be a problem (not that I expect that to occur) – before following the Fed slowly higher as AI-related inflationary pressures continue to keep inflation above target. Interest rate cuts next year are not in my current scenario and would require much weaker job advertising trends and NAB business conditions prints.