Perpetual Markets Economics and Interest Rate Commentary – 11 May 2026

The economic outlook remains hostage to Middle East developments, but the AI boom continues in the background.

Key points

- The near-term economic outlook remains hostage to geopolitical events in the Middle East, albeit with a supportive, but inflationary boost coming from continuing significant AI spending.

- A quick resolution to the Middle East conflict would likely see a more positive activity scenario re-establishing, while an extended closure would portend less favourable economic conditions, albeit with the supportive AI backdrop continuing.

- The former scenario could see a long, slow tightening cycle in Australia, while the latter would see less reason to tighten further (it’s the combination of oil prices and interest rates that is important).

- This week’s Australian budget promises to be a bit more interesting than in recent years, with significant tax changes and spending cuts rumoured. The budget should be judged on the extent to which decisions place the Government’s finances on a more sustainable medium-term footing and are fair and equitable, against the extent to which further cost-of-living support makes the RBA’s job more difficult in the near-term. It’s important any such support measures are targeted and temporary.

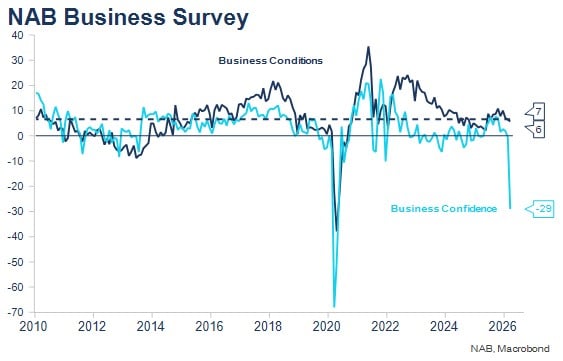

- The NAB Survey will be closely watched to see the impact of higher oil prices on business conditions, which were quite resilient in March, but also for readings on the extent and speed of pass through of higher energy into input costs and retail prices.

- The Wage Price Index is not expected to be market moving. It’s important that the upcoming minimum wage decision at this stage does not build in a higher wage outcome for energy price developments that may not be sustained.

- I continue to expect US markets to factor in the risk of higher interest rates like other markets around the world. This reflects strength in equity markets and emerging inflationary pressures even before the Middle East conflict.

The week ahead – key Australian and US events (including Budget preview)

Tuesday 12 May: NAB Business Survey (April); Australian Federal Budget 2026-27 (7.30PM); US CPI (April).

Wednesday 13 May: Wage Price Index (Q1).

Thursday 14 May: US Retail Sales (April).

Friday 15 May: US Manufacturing Capacity Utilisation.

There are also speeches from six different Fed officials, which will no doubt cast more light on the debate about whether to shift to a neutral bias. Collins (a non-voter this year) revealed last week that she favoured a shift to a neutral bias at the last meeting. Williams' speeches are always interesting. He often tends to represent the “centre” of FOMC views.

The NAB Business Survey should show some recovery in business confidence given the moderate reduction in oil and diesel prices over April. This was importantly due to significant but temporary government support. Business conditions are likely to deteriorate after last month’s surprising resilience. Conditions are typically a more reliable signal than confidence. The current divergence likely highlights the bookend outcomes for the economy between a quick Middle East conflict resolution (confidence recovers towards conditions as pre-existing conditions re-establish) and an extended Strait of Hormuz closure (conditions converge toward confidence under far less favourable economic conditions).

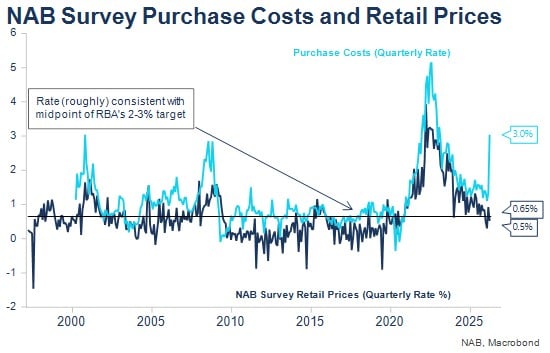

The markets and RBA will be keenly interested in the input and retail price readings as a gauge for the speed and extent of fuel price pass through (what the RBA appears to be deeming second-round effects, but effects the Governor noted cannot be impacted by monetary policy actions now. Interestingly, the RBNZ Governor would deem these indirect first-round impacts). Input costs rose at the fastest pace ever last month, reflecting both the size of the fuel price increase and the broad-based impacts of energy prices in transport and production processes.

The 2026-27 Federal Budget is shaping up to have a bit more spice than recent budgets, with the Treasurer likely to announce changes to tax arrangements for housing and trusts along with significant spending savings, much from changes to the NDIS.

As in previous years, many aspects of the budget have been leaked. An interview with the Treasurer in the weekend press highlighted the following five major policy priorities:

- Fuel Security.

- Cost of Living and Intergenerational Housing Equity.

- Productivity.

- Tax Reform.

- Savings.

Economists will be critical of further cost of living support, which does add to demand and makes the RBA’s task controlling inflation somewhat harder. It will be important that any further support is targeted and temporary, as the Middle East conflict could soon end. It’s hard to argue with efforts to improve productivity or to increase savings and cut or reprioritise spending. The tax reform package is likely to be contentious given it seems it may introduce changes to the capital gains tax discount and negative gearing for housing, measures that saw then Labor Party leader Bill Shorten defeated at the 2019 election. Some changes to trust taxation seemed overdue.

The critical judgement about the budget will be to weigh up the extent to which decisions are made to put Federal Government finances on a more sustainable footing over the medium-term against the extent to which further cost of living support might add to the RBA’s task in the near-term.

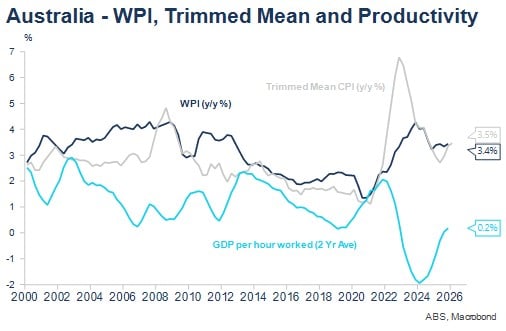

The Wage Price Index is expected to record another quarterly increase of 0.8%, bringing the annual rate of change to 3.3% (a touch lower than last quarter). With Australian productivity growth weak in recent years, that’s still a little high to be consistent with 2.5% inflation. The continuing low unemployment rate has seen the SEEK advertised wages series strengthening a little in recent times, which argues against a downside surprise. It’s important that the Fair Work Commission does not make an additional wage grant to compensate for higher fuel prices, at least at this stage, as these hopefully will turn out to be largely temporary.

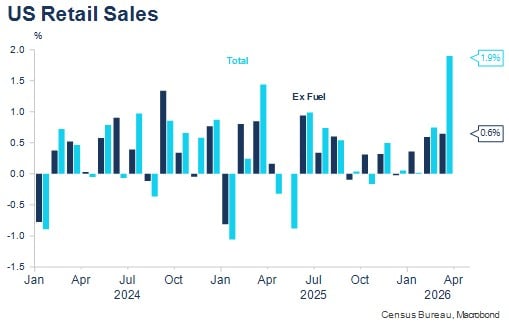

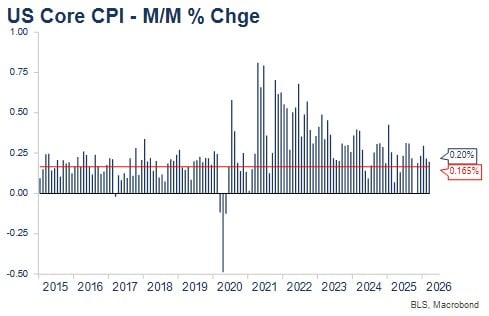

In the US, the focus will be on April Retail Sales data (to see the impact of the Iran conflict on non-energy spending), as well as the April CPI (to monitor for pass through of energy prices into retail prices). Economists are forecasting headline retail sales to increase a further 0.6%, while ex Autos and Gas Retail Sales are expected to rise 0.4% m/m. The monthly core CPI is expected to tick higher from 0.2% m/m in March to 0.3% m/m in April and from 2.6% y/y to 2.7% y/y. A group in the Fed had been judging inflation as close to target excluding the one-off impacts of tariffs, allowing focus on the labour market data. Aspects of the energy price surge will also be treated as one off, though some members worry about the cumulative effect of a series of one-off shocks on inflationary expectations, and the Fed Pressure Index was showing a degree of inflationary pressure emerging even before the Iran conflict, reflecting the AI boom.

Middle East developments and chart review

Another week and the Strait of Hormuz remains closed. Oil prices however are around 10% lower over the week, with Brent around US$100pb. This reflected continuing negotiations between the US and Iran, with the US proposing a fourteen-point peace plan. The media is reporting Iran’s response over the weekend as including an end to the war in Lebanon, the unfreezing of all Iranian assets globally and removal of all restrictions on Iranian oil exports, along with discussions surrounding the control of navigation rights in the Strait of Hormuz. There has been little mention of how Iran’s nuclear program may develop. The proposal seems unlikely to be accepted by the US and weekend oil prices were 2.5% higher on IG Markets.

US share prices continued to advance on better-than-expected Q1 earnings outcomes; optimism regarding both AI spending and medium-term AI-related profitability developments, rising 2.3% over the week. That’s still a reminder of the double shocks impacting the world economy presently and of the cushioning effect of AI spending on growth, despite much higher oil prices. If resolution in the Middle East can be reached, I’m expecting the re-establishment of the emerging stronger global growth scenario.

The RBA surprised me by moving a little earlier than I expected to increase interest rates again. While the case was clear from a domestic inflationary perspective, I thought the uncertainty about the Middle East might see the Board hold off for a further six weeks. In the event, the Governor’s post-Board press conference seemed to indicate that with policy now seen as a little restrictive, the Board considers it has done enough in the short term to give it some space to observe how events unfold in the Middle East, how price pass through occurs and how the economy reacts to the three interest rate increases recently implemented.

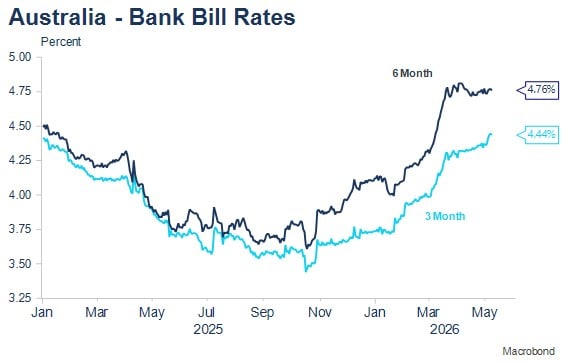

Six-month yields were little changed over the week as a result. The market continues to price just under one and a half further interest rate tightenings. There is a 20% chance of a rate rise in June priced (I expect no change), a 75% chance of a further increase at the August meeting, with a further rise fully priced by the September meeting. Peak pricing occurs at the February meeting next year.

A further rise in August seems likely if oil prices remain around current levels or decline. My thinking remains that it’s the combination of oil prices and interest rates that is important. The higher oil prices rise, the less likely the need for further near-term interest rate rises.

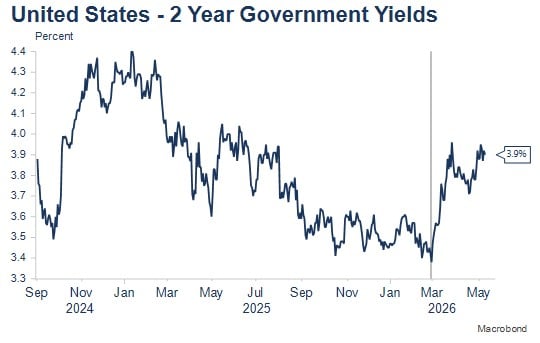

US 2-year yields meanwhile, were relatively unchanged over the past week, though US markets continue to slowly follow other markets in pricing in the prospect of rises in short-term interest rates. The US market now has a full rate rise priced by the April 2027 meeting but retains a very mild chance of easing at the next few meetings. I expect further tightening to be priced in by US markets.

Australian economic and interest rate scenarios

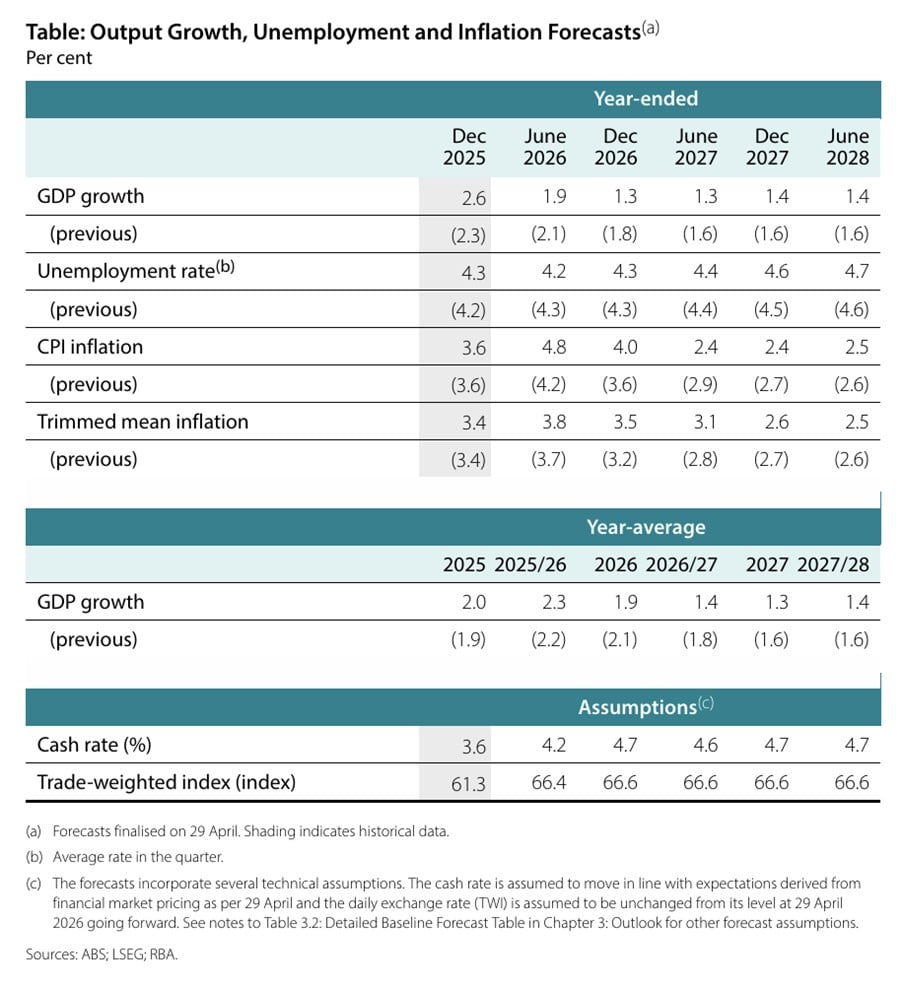

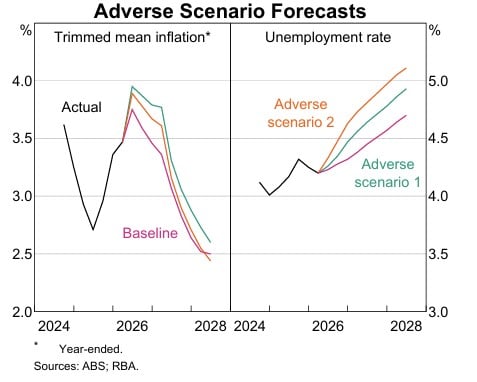

The RBA’s May Statement on Monetary Policy sensibly contained scenarios for the economy under a range of potential outcomes for the Middle East conflict and oil prices, and the unknown impacts on growth and inflation. The core scenario assumes the conflict is resolved very soon, there is one and a half further interest rate rises (market pricing) and oil prices fall back over the remainder of the forecasting period as suggested by market pricing. Futures market pricing for oil has shifted higher, in part reflecting assumptions by the market that it will take some time for full Middle East capacity to come back online.

The core scenario sees the economy slow further below trend growth, inflation sharply higher in the near term but moderating back to target at end 2027, and the unemployment forecasts a little strangely, not particularly impacted.

The two adverse scenarios modelled both include an extended Strait of Hormuz closure for the remainder of 2026. Under both scenarios, oil prices rise to US$145pb in Q2, but then gradually decline to US$90/95pb over the remainder of the forecast period.

The difference in the scenarios are the responses of inflation (more persistent in adverse scenario 1) and the impact on demand (more impacted in adverse scenario 2). To me, these Strait of Hormuz closure scenarios would produce more adverse oil price and economic growth outcomes.

The chart shows the higher unemployment outcomes that are expected for both adverse scenarios that are expected by the RBA, though again, the impact on unemployment seems relatively small for the shock. My expectation is that a sustained US$145pb oil price would likely cause global recessionary conditions. No scenario assumes that oil supplies are interrupted, which would likely cause additional interruptions to activity similar to those which occurred during COVID lockdowns.

Interestingly, the RBA’s scenarios do not consider the potential for a more positive outcome, one where a quick resolution is reached and oil prices return relatively quickly to pre-conflict levels. This scenario would likely see the more positive bias to global economic growth that was evolving due to the AI investment boom, re-establish, with positive spillovers in the near term for selected parts of Australian mining. That scenario would likely see the emergence of a long, slow tightening cycle in Australia, akin to that which occurred during the mid-2000s mining boom.